The Weekly Docket

By Louis Lehot, Partner, Foley & Lardner LLP. Garage to global, since Y2K. #AskASiliconValleyLawyer · Vol. I, No. 22 · May 23, 2026

Friends,

Long enough in this business to remember when an IPO meant a paper prospectus and a fax machine. This week brought the largest S-1 in history, a seed round our team led, a public offering, and a regulator who thinks it just fixed the IPO market. It didn’t. Here is the docket.

Last Week (May 18 to 22)

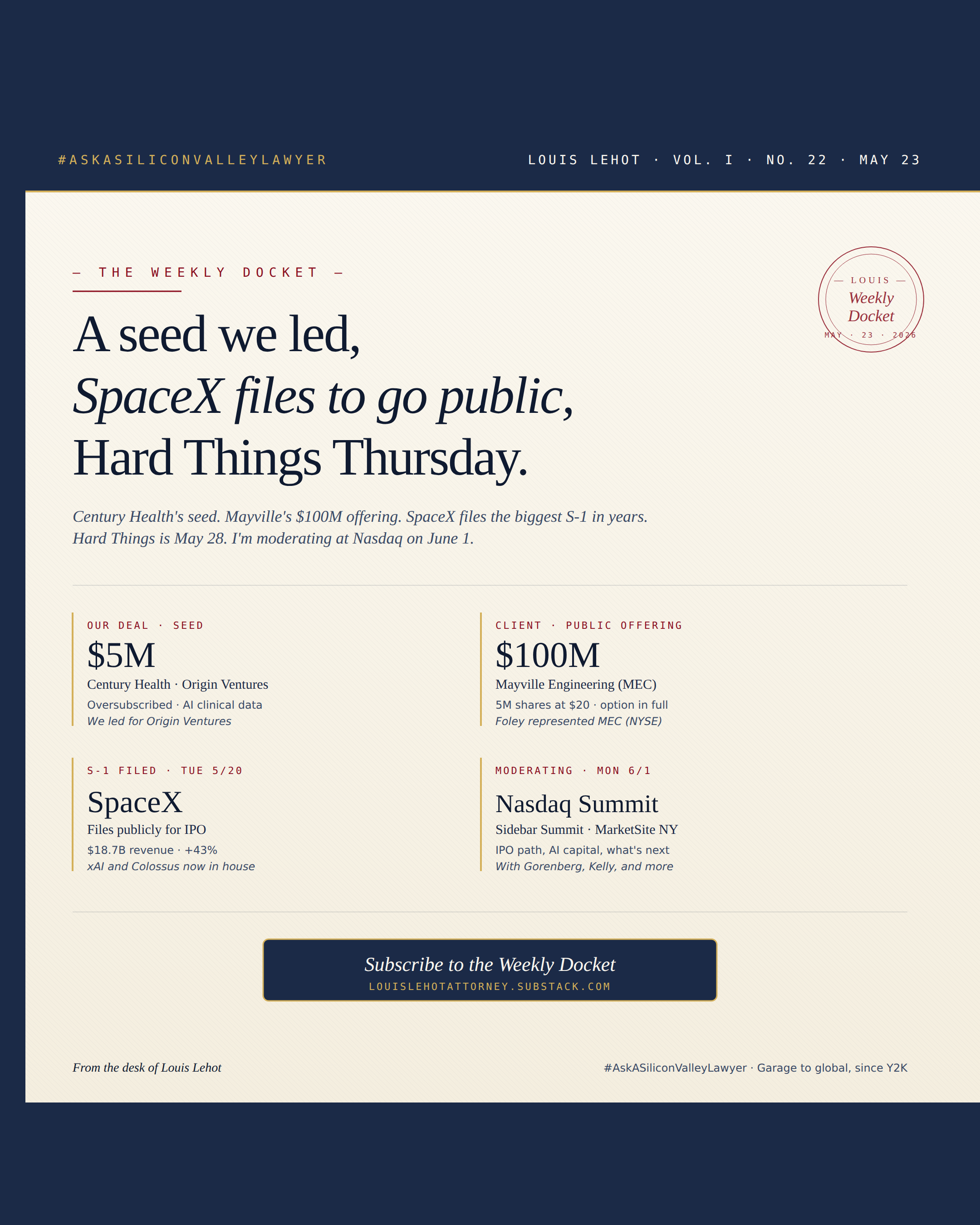

Our team represented Origin Ventures as lead investor in the $5M oversubscribed seed round for Century Health, which uses AI to turn fragmented clinical data into real-world evidence for therapeutic development. A word for anyone investing in clinical-data AI: the model is not the moat, the data rights are. Who owns the data, what consents travel with it, and whether you can commercialize the evidence are the three questions that decide the investment. Ask them before the wire, not after.

Foley represented Mayville Engineering Company (NYSE: MEC) in its $100M public offering. Five million shares at $20, with the underwriters exercising their option in full for another 652,000. Mayville makes its money in the physical world, building metal components for commercial vehicles, datacenters, agriculture, and the military. When a manufacturer with real datacenter exposure can tap the public markets cleanly in this tape, the offering prices itself.

Foley is advising Kontoor Brands (NYSE: KTB) on the sale of its Lee business to Authentic Brands Group. Carving a single brand out of a public multi-brand company is its own art form: the glamour is in the press release, the work is in the transition services agreement, and the value sits in the IP licensing schedules. Read the boring documents. The boring documents are never boring.

Foley represented EMS, a Wynnchurch Capital portfolio company, in its acquisition of American Metals Supply. Aluminum distribution for the patio and industrial markets. That will not trend on X. But sponsor-backed roll-ups in unglamorous sectors are quietly producing some of the best risk-adjusted returns in private equity right now, precisely because nobody is writing breathless threads about aluminum. Not every great deal needs a GPU. Some just need a loading dock.

SpaceX filed its S-1 publicly on Tuesday, the largest filing the markets have seen in a generation. Strong headline numbers, $18.7 billion in 2025 revenue, up 43%, with positive adjusted EBITDA in the first quarter. But the part that should interest every deal lawyer is the AI business. The February acquisition of xAI and the Colossus compute infrastructure means frontier AI and the largest training cluster on the planet now sit inside the entity going public. That is the bold move: a space and connectivity company reintroducing itself as one of the most serious AI infrastructure platforms in the world, in the open. The governance matches the ambition, a dual-class structure that keeps founder control intact through the transition, exactly right when the plan is measured in decades. Read the S-1 for the AI strategy alone.

The venture tape stayed warm even as M&A cooled. Decart raised $300M, Exa $250M at a $2.2B valuation, Mercury $200M at $5.2B, and Socket hit a $1B valuation on a $60M round. The part that does not photograph well is M&A, where deal volume has slowed two months running against last year. The reason is not rates or some macro bogeyman. It is that nobody can agree on what enterprise software is worth anymore. Claude Code and the AI-native wave are not eating startups, they are eating SaaS. The seat-and-renewal software business is under pressure, because a buyer can no longer tell whether a target’s recurring revenue is durable or about to be rebuilt in a weekend by three engineers and a coding tool that did not exist eighteen months ago. The seller is anchored to last year’s multiple, the buyer sees a commodity, and the gap is where deals go to die. One correction to the conventional wisdom: reps and warranties insurance is not getting more expensive, it is getting narrower. Underwriters are adding exclusions, so the protection you think you bought may not be there when you need it. Identify and mitigate the liability before the process begins, because the carrier will not backstop what you missed.

On immigration, the war on legal, high-skilled talent is the most self-defeating policy I have seen in a generation. Let me be clear about what this is, because the word “immigration” is doing a lot of hiding. This is not about the border. This is a deliberate assault on the legal, vetted, highest-skilled people on earth, the founders and engineers and scientists who apply through the front door, follow every rule, and build the companies that keep this country ahead. Half the great firms in this valley were started by someone who arrived on a visa. We are now telling the next generation of them that they are the problem. Forcing a founder to leave the country and return to a home-country consulate to convert an H-1B into a green card is not paperwork, it is a loaded gun pointed at the company, because the person who flies home may simply not be allowed back. Add the $100,000 fee on a new application and you have not built a merit filter, you have built a tax, and it falls hardest on the seed-stage startup that can least afford it while the largest incumbents shrug and write the check. The rest of the world is not standing still. Canada, the United Kingdom, France, and the Gulf are rolling out the welcome mat for exactly the people we are turning away, and they are not subtle about why. If we are serious about winning the AI race, the single most valuable resource in it is human talent, the smartest people in the world, and we should be competing to keep every one of them here. Instead we are showing them the door and calling it strength. It is not strength. It is an own goal of historic proportions, and we will spend the next two decades watching the companies we should have hosted get built somewhere else. Stop charging admission to the people who built this place.

And the SEC proposed reforms I wish I could be more excited about. Monday’s rulemakings under Chairman Atkins’s “Make IPOs Great Again” banner give us a 60-month IPO on-ramp, the end of the 12-month S-3 seasoning requirement, and extended emerging-growth-company accommodations, on top of the May 5 semiannual reporting proposal. These are fine. They are nowhere near enough. The number of public companies has fallen by roughly 40% since the 1990s, and not because the 10-Q was too frequent. The whole architecture of going and staying public stopped making sense while private capital got deep enough that nobody had to bother. You do not fix that with a longer on-ramp. You fix it by making the private markets play closer to public rules once a company is systemically significant. Reinstate the 500-holder registration trigger the JOBS Act gutted in 2012 when it raised the threshold to 2,000. Then go further: require any private company that has raised $1 billion or more to publish audited financials. If you have taken that much money from that many people, you are a public company that has not admitted it yet. That is rearchitecture. A gentler filing calendar is decoration. I will file a comment letter before the July deadline anyway, because silence is not advocacy.

From Where I Sit

Enough complaining for one issue. The mood on the ground is the best it has been in years.

San Francisco is back. The neighborhoods that two years ago looked like a zombie film, papered windows and that particular silence a city makes when the money leaves, are full again. AI capital is pouring into exactly those blocks. The offices are lit at night, people are out, and there are lines outside coffee shops that were boarded up not long ago. This city keeps roaring back the moment its obituary is typed. There has never been a better time to build here.

Which is why the policy has to keep up, and here California is its own worst enemy. You cannot host the most important technology boom in a generation and treat the people creating the value as a piggy bank. The answer to a budget gap is not another tax on companies and talent that can increasingly build from anywhere. Texas and Florida have spent a decade making that case for us. Lower the cost of staying, or hand away the edge we currently enjoy.

And enough with the AI apocalypse. The doom narrative has become an intellectual costume, a way to sound serious by predicting catastrophe, and it misses what is actually happening. The best work crossing my desk is AI for good: pulling evidence out of the medical record so patients get better therapies faster, catching disease earlier, letting a small team do what used to take an army. Technology is a mirror. The founders I represent are not building Skynet. They are building things that make people healthier and work more humane. That is the story worth telling, and the one I am betting on.

On the Calendar

◊ Hard Things Round Three. Thursday, May 28, San Francisco. Our invite-only Physical AI evening with Vitaly Golomb and Mavka Capital. Round One was Veena Radhakrishna of Cartesian Kinetics, Round Two was Andra Keay of Silicon Valley Robotics, and Round Three keeps the bar where we like it. If you build, fund, or advise in robotics, autonomous systems, or embodied AI, reply and I will save you a seat.

◊ Foley at Boston Tech Week and NY Tech Week. Out in force at both. If you want to find each other in the scrum, reply.

◊ Sidebar Summit at Nasdaq. Monday, June 1, New York. I am moderating the 3:00pm panel at Nasdaq MarketSite, less a panel than a boardroom conversation with an audience: the path to the public markets, AI as the dominant capital category, and where innovation clusters. Joining me are Mark Gorenberg (Zetta Venture Partners, Chairman of the MIT Corporation), Chris Kelly (investor across AI, blockchain, and infrastructure), and others. No slides, no filler, no mercy. Register here.

◊ Secondaries Forum. Tuesday, June 9. Tender offers, GP-led secondaries, continuation vehicles, and the practitioners actually closing them. With the IPO window open but companies staying private longer than planned, this is the liquidity conversation that matters. Reply for details.

Closing Argument

◊ Carving out a brand or division: the transition services agreement is the deal. Staff it like one.

◊ Selling this year: reps and warranties insurance is narrowing, not just repricing. Mitigate liability before the process begins, because the carrier will not backstop what you missed.

◊ Eyeing the public markets: SpaceX gave a clinic in telling a multi-business story in one prospectus. Study it, then get your readiness memo, 10b5-1 program, and independent directors in place.

◊ Hiring specialized talent: the assault on legal, high-skilled immigration is real. Budget for the $100,000 H-1B fee and the genuine risk that a founder sent home to convert a visa is not let back in. Plan around a system now working against you.

◊ Waiting on the SEC: do not hold your breath. The real fix is the 500-holder rule and forced disclosure for billion-dollar private companies, not a longer on-ramp.

◊ Deciding where to build: San Francisco is genuinely back. Just keep an eye on Sacramento.

— Louis

#AskASiliconValleyLawyer #FoleyIgnite #garage2global #SiliconValley #ai #ipo #venturecapital #mergersandacquisitions #physicalai #techlaw

Standard disclosures: opinions my own, not my firm’s. Not legal advice. Attorney advertising. Prior results do not guarantee a similar outcome.

pinning "the boring documents are never boring". great issue louis